(Image via

(Image viaOwning a luxury car is a goal for many people. The allure of a prestigious badge, premium materials, powerful performance, and cutting-edge technology is hard to resist. The experience of driving a high-end vehicle can be truly special. But the dream of ownership often focuses on the purchase price, while the real, ongoing costs are overlooked. The sticker price is just the entry fee. The true cost of luxury car ownership is revealed over years of maintenance, insurance, depreciation, and fuel expenses. Understanding these hidden costs is the key to enjoying your premium vehicle without it becoming a financial burden. This guide will break down the real costs and offer practical ways to manage them.

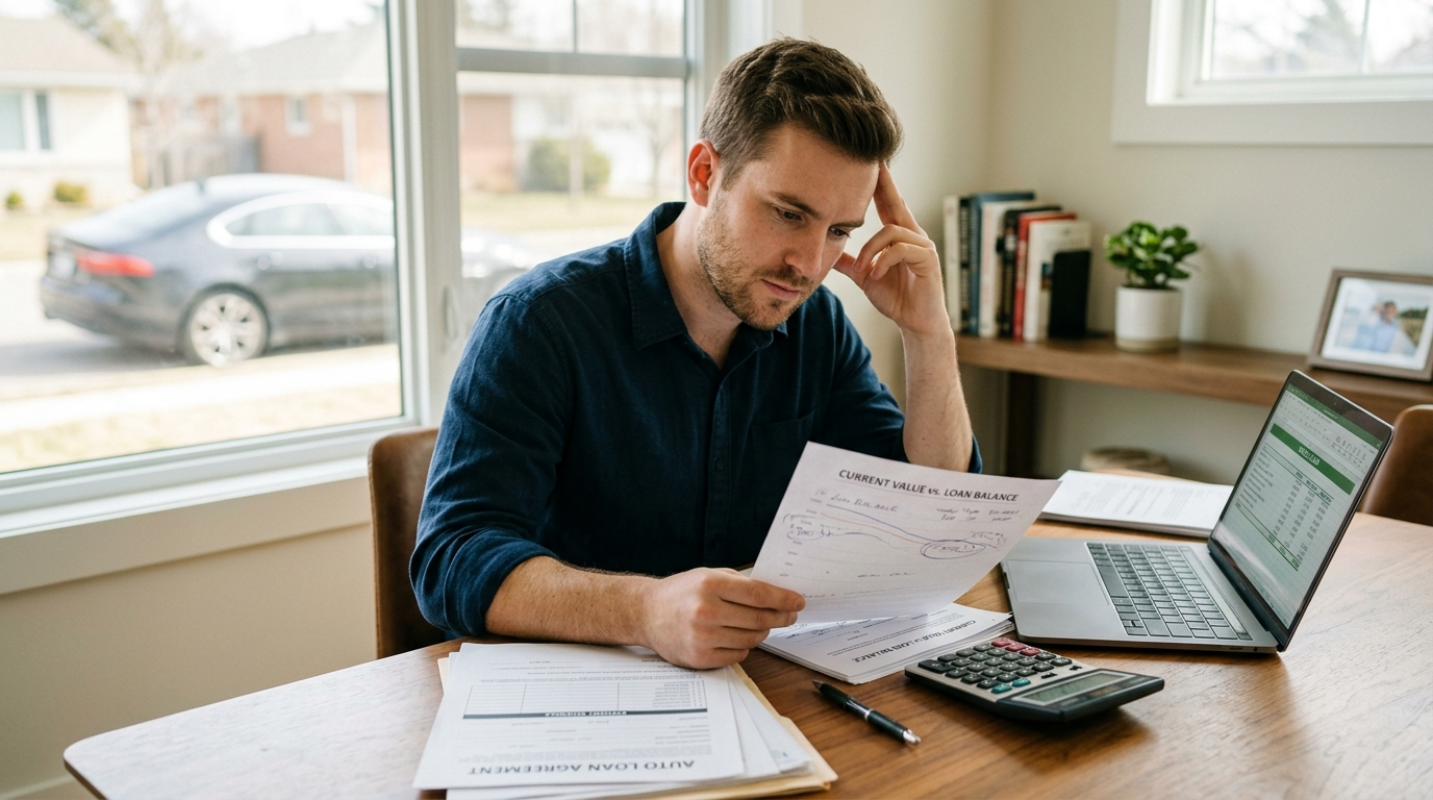

Depreciation is a Big Issue

Depreciation is the decline in a car's value over time, and it is the single largest expense for almost any new car owner. Luxury cars are hit particularly hard by depreciation. Their high initial price means there is more value to lose, and the rapid pace of technological updates in the premium market can make older models seem dated more quickly. A standard car might lose around 40-50% of its value in the first three years, but a luxury car can easily lose 50-60% or even more in the same period.

A $90,000 luxury sedan could be worth less than $40,000 after just three years. That is a loss of over $50,000 in value, or nearly $1,400 per month. This "invisible" cost is something you don't pay out of pocket each month, but it has a huge financial impact when you decide to sell or trade in the vehicle.

How to Manage Depreciation

- Buy Certified Pre-Owned (CPO): The smartest way to fight depreciation is to let someone else take the biggest hit. A two or three-year-old CPO luxury car has already gone through its steepest period of value loss. You get a vehicle that is still modern and in excellent condition, often with a manufacturer-backed warranty, for a fraction of its original price.

- Choose a Model with Strong Resale Value: Not all luxury cars depreciate at the same rate. Brands like Porsche and Lexus are known for holding their value better than others. Research the projected resale value of the models you are considering before you buy.

- Lease Instead of Buy: Leasing allows you to sidestep the long-term effects of depreciation. Your lease payment is based on the car's expected depreciation during the term you use it, not its full purchase price. This provides a predictable cost and lets you move on to a new vehicle after a few years without worrying about resale value.

Premium Costs for Maintenance and Repairs

Luxury cars are built with advanced engineering and high-end components, which means that maintaining and repairing them is more expensive. Everything from a simple oil change to a major repair will cost more than it would on a non-luxury vehicle. The parts are more expensive, and the labor rates at specialized dealership service centers are higher because technicians require specialized training.

An oil change for a standard car might cost under $100, but for a high-performance luxury car, it can easily be $250 or more. Brakes, tires, and other common wear-and-tear items are also significantly pricier. A new set of high-performance tires for a premium SUV could run well over $1,500. When the factory warranty runs out, an unexpected repair, like a problem with the air suspension or infotainment system, can result in a bill for thousands of dollars.

How to Manage Maintenance Costs

- Look for an Independent Specialist: Once your car is out of warranty, you don't have to go to the dealership for every service. Find a reputable independent mechanic who specializes in your car's brand. Their labor rates are often lower than the dealership's, and they can provide excellent service.

- Consider an Extended Warranty: If you plan to keep your luxury car beyond its factory warranty period, an extended warranty can provide peace of mind. It can protect you from huge, unexpected repair bills. Be sure to shop around for these warranties, as you can often buy them from third parties for less than the dealership's offer.

- Stay on Top of Routine Maintenance: Following the manufacturer's recommended service schedule is the best way to prevent small issues from turning into major, expensive problems.

High-Octane Fuel Requirements

Most luxury and high-performance vehicles require premium fuel (91 or 93 octane) to run correctly. The high-compression engines in these cars are designed for higher-octane fuel to prevent engine "knock" and achieve their advertised horsepower and fuel efficiency. Premium gas can cost 50 to 80 cents more per gallon than regular unleaded.

If you drive 15,000 miles a year in a car that gets 20 miles per gallon, you will use 750 gallons of gas. The extra cost for premium fuel could add up to an extra $375 to $600 per year compared to a car that runs on regular. This might not seem like a massive amount on its own, but it is another piece of the ownership cost puzzle.

How to Manage Fuel Costs

There is not much you can do about the requirement for premium fuel, but you can be mindful of your driving habits. Aggressive driving with rapid acceleration and hard braking hurts fuel economy. Driving smoothly can help you get the most out of every expensive gallon.

Costly Car Insurance Premiums

Insuring a luxury car costs more for several reasons. The car's high purchase price means it is more expensive for the insurance company to replace if it is stolen or totaled in an accident. The high cost of parts and specialized labor also means that even minor collision repairs are more expensive. Finally, some luxury sports cars are seen as higher risk due to their powerful engines. All these factors lead to higher insurance premiums. The difference can be substantial, with insurance for a luxury vehicle often costing hundreds or even thousands of dollars more per year than for a standard car.

How to Manage Insurance Costs

- Shop Around: Insurance rates for the same car can vary significantly between different companies. Get quotes from at least three to five different insurers before you make a decision.

- Ask for Discounts: Make sure you are getting all the discounts you qualify for. These can include discounts for being a good student, having multiple policies with the same company (bundling home and auto), or having a clean driving record.

- Choose a Higher Deductible: A higher deductible—the amount you pay out-of-pocket before your insurance kicks in—will lower your monthly premium. Just be sure you have enough in savings to cover the deductible if you need to make a claim.